Financial Contract-for-Differences

A modified CfD preserving the market price incentive.

"Details matter. It's worth waiting to get it right." - Steve Jobs, Founder of Apple

When embarking on the design of any modification to a system, it becomes imperative to grasp the potential ramifications of such alterations. This principle holds true when introducing a novel support scheme for renewable energy sources. The key inquiry that necessitates attention is whether this support scheme seamlessly aligns with the existing electricity market model.

In this article, our focus is not to delve into every facet of the Contract-for-Differences (CfD) but to scrutinize a pivotal aspect: its interaction with market price incentives. Let's delve deeper into this intricate relationship.

This post has been summarized in the following Twitter/X thread.

The EU push for CfDs

The European Union has recently decided that Contract-for-Differences (CfD) would be the mandatory support mechanism to support investments in new renewables and new nuclear energy:

The Council agreed that two-way contracts for difference (long-term contracts concluded by public entities to support investments, which top up the market price when it is low and ask the generator to pay back an amount when the market price is higher than a certain limit, in order to prevent excessive windfall profits) would be the mandatory model used when public funding is involved in long term contracts, with some exceptions.

Two-way contracts for difference would apply to investments in new power-generating facilities based on wind energy, solar energy, geothermal energy, hydropower without reservoir and nuclear energy. This would provide predictability and certainty.

In addition, there is a possibility to use this mechanism for lifetime extension of existing assets, which would mean that practically, it could be used for existing nuclear power plants. This point was a key part of the disagreement between France and Germany.

Since CfD seems to be the tool that would be largely used across Europe, it is of uttermost importance to understand correctly the mechanism and to implement it in the most optimal way.

What is a CfD?

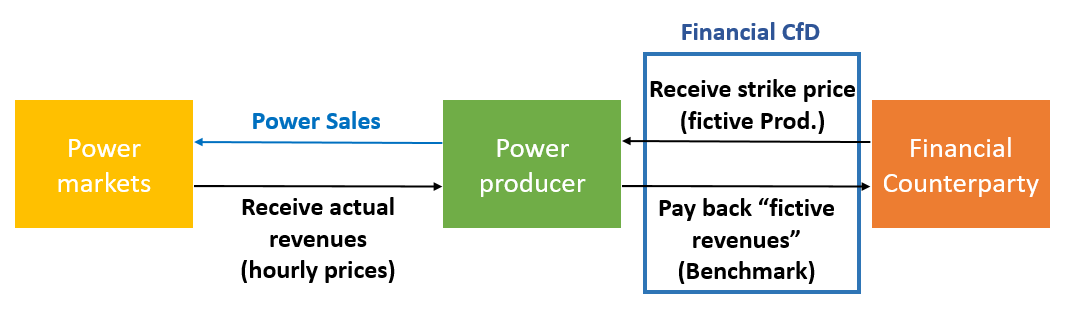

We explained the mechanism of a CfD in a previous post. In a nutshell, a CfD is a long-term contract between a power producer and a financial counterparty compensating the difference between the sale price of electricity and an agreed price (the strike price). Therefore, the power producer will be subject to two financial streams:

The sale of electricity to the electricity markets.

The difference between a predetermined strike price, typically established through a competitive auction and remaining constant over time, and a reference market price, generally the day-ahead market price.

In case, the strike price is lower than the market price, the generator must pay the difference to the counterparty, and vice-versa.

Such a mechanism ensures the generator a fixed revenue as the price of the electricity sales is compensated by the financial counterparty, which is generally a public company1.

The issue with the “regular CfD"

The CfD mechanism increases the bankability of new-generation projects as the revenues do not depend on the market prices. Since the projects are more secure and therefore more attractive, new projects would most probably be cheaper as the premium for the market risk does not exist.

Nevertheless, a CfD is removing the market price incentives and is pushing generators to produce independently of market prices. Indeed, with a CfD, the generator is ensured to receive a fixed amount per kWh produced as the difference between the market price and the strike price is compensated exactly. In that sense, a CfD is comparable to a Feed-in Tariff in which the buyer resells all the generation on the market. With the absence of a market price incentive, the main objective of generators is to produce as much as possible, and not to catch the most market value.

A usual add-on has been to annul the payments to generators if market prices turn negative for a number of consecutive hours. This is a first good step but it is certainly not sufficient as it only removes the incentive to produce during the hours with negative prices.

The question is open: is there a way to keep the attractiveness of the CfDs (secure financial flows) while keeping the price incentive?

A solution: decoupling payments from actual generation

One potential solution is the concept of "financial CfD”. In this post, we will focus on one particular aspect, namely the decoupling of the actual generation of the power plant from the payments to the power plants. Several people have already discussed this topic, such as this paper, which provides a more in-depth analysis.

The core principle is that the financial transfers (either positive if the strike price is above market price or negative otherwise) are based on a benchmark2, linked to the production technology. For example, to support a solar power plant in Belgium, we can take as a benchmark the average production of solar in Belgium. We could also imagine different benchmarks such as the “Capability-based CfD3”.

The financial flows with a financial CfD would then be similar to a regular CfD except that the financial flows between the power producer and the financial counterparty will only be based on the “fictive production” of the benchmark.

It should be noted that in case the producer does not modify its market behavior compared to a situation where he receives a regular CfD4, his production would be similar to the benchmark, and therefore the financial CfD and the regular CfD are identical. This is why we can see the financial CfD as the combination of a regular CfD and a market incentive to “beat the benchmark”.

So, the objective of the financial CfD is to keep the market incentives on generators and therefore, to modify the market behavior compared to a regular CfD. But is it really needed? Let’s explore why and how.

Does it matter for wind and solar?

Even though we cannot control the wind and the sun, we still have some options to modify the production of renewables to make them more “market-friendly”. Let’s take an example of when a solar operator must conduct maintenance on a specific week. Hereunder, the first graph shows the forecasted production (in MWh per hour, or MW) over three days as well as the realized market prices (€/MWh, the blue curve). The second graph shows the value of the production in €. We can observe that the first day has less production compared to the last day, but the market value of the first day is much higher than the last day. This is caused by a drop in market prices due to the solar cannibalization effect.

With a regular CfD, the incentive for the producer is to produce as much as possible, and therefore, he will choose to perform the maintenance on the first day (green box, the day with less production). With a financial CfD, as it is based on a benchmark and not his own generation, the producer will be incentivized to perform the maintenance when the market value is the lowest (pink box).

With a financial CfD, the focus of the producer will shift from producing the most energy to producing the most value for his generation. This shift might lead the producer to select different equipment and organize his operation in a different manner5. In addition, the producer would have to take a more active role in electricity trading.

A simplified version: regular CfD with different strike prices

We could also imagine another solution to modify the market behavior of generators: a regular CfD with two or more strike prices. For example, if the strike price during sunny hours is set lower, the generator will be incentivized to maximize the generation during the hours with the higher strike price.

This modification is nevertheless not so simple to implement practically: which hours should be selected? What would be the difference between the low and the high strike prices? Market prices are dependent on many variables and it is impossible to forecast how market prices would be in the coming years6.

What about nuclear?

The CfD has also been contemplated for nuclear energy, particularly as a potential substitute for the ARENH7 in France. While nuclear power is commonly perceived as inflexible and characterized as a baseload asset, this perception is not entirely accurate. This flexibility can be exemplified below. In fact, when market prices are low, operators of nuclear power plants may decrease their generation output.

In a traditional CfD framework, operators are incentivized to maximize their generation output, which eliminates any market-driven motivation for such modulation. However, in the context of a financial CfD with a benchmark defined as a baseload, operators can still retain market incentives.

In conclusion

Contract-for-differences stand out as a powerful instrument for ensuring the bankability of renewable energy assets by guaranteeing revenue streams over an extended period. This, in turn, mitigates project risks and ultimately reduces overall project costs. However, as the prevalence of renewables grows, their influence on market prices becomes increasingly significant. Hence, it becomes imperative to shift the focus for renewables from maximizing total production to maximizing total value8.

Financial CfDs present a compelling solution by preserving market incentives while still ensuring adequate revenues. Nevertheless, it's important to acknowledge that this is just one facet of a broader strategy, and additional measures, such as investing in power grids and energy storage, are indispensable to mitigate the risk of price cannibalization.

For a more in-depth exploration of financial CfDs, we recommend delving into the comprehensive insights provided in this research paper, which offers a wealth of detailed information on the topic.

In the UK, this financial counterparty is the Low Carbon Contracts Company.

Defining correctly the benchmark is not the scope of this post but it is extremely important to ensure a proper mechanism.

In a Capability-based CfD, the benchmark is the potential production of the considered generator itself.

With a regular CfD, the producer is incentivized to produce as much as possible, independently of the market value.

A solar farm could change the orientation of the panels for example. The AC/DC ratio might be different as well.

A CfD is generally signed for 15 years.

When the penetration of renewables was low, the impact on prices was negligible and therefore, maximizing production was a good proxy for maximizing value.

Hi Julien,

I was wondering how power producers time their maintenance programs in order to capture the maximum value of the market. Don't they need to do extensive planning to carry out maintenance work? Also, I'm curious to know how far in advance power producers can predict power market prices to schedule their maintenance so that it's both feasible and financially viable.

Hi Julien.

A relatively simple option is to have the strike price linked to a medium term average (monthly seems to be the most practical). This means that projects bear the cannibalisation effect and have to be market-responsive in the short term and do profile optimisation to the extent they can