Germany under the sun

Graphs, insights and reflections on solar (with data up to May 2024)

We are now in mid-June, the peak period for solar energy generation. After analyzing market dynamics over the first five months of the year, I found it interesting to present some graphs illustrating the impact of solar energy in Germany and propose some reflections. The larger impact of solar this year is unsurprising given that while demand has remained relatively stable over the past year, solar capacity has continued its rapid progression. Meanwhile, flexibility in the energy market has not increased at the same rate, making it clear that solar is set to mark 2024 (and the years to come).

Let’s explore.

The rapid rise of solar

The rise of solar has been spectacular. Here is an abstract from the Global Electricity Review 2024 of Ember.

Solar is leading the energy revolution. It was the fastest-growing source of electricity generation for the 19th year in a row, and surpassed wind to become the largest source of new electricity for the second year running. Indeed, solar added more than twice as much new electricity as coal in 2023. The record surge in installations at the very end of 2023 means that 2024 is set for an even larger increase in solar generation.

The graph below illustrates global growth, showing no signs of slowing down. We can anticipate 2024 to set new records.

Zooming in on Germany, we observe a different trend. Solar energy experienced a massive boom at the beginning of the last decade, primarily driven by substantial subsidies for rooftop solar installations. These subsidies, valid for 20 years, are still being paid today1. This financial support not only boosted domestic capacity but also played a crucial role in accelerating global cost reductions.

Recently, the rate of installed capacity in Germany has surged again, especially since 2023. The country is now installing more than one gigawatt of solar energy each month—a level that, in 2014, took an entire year to achieve. To meet its target of 215 GW by 2030, Germany needs to maintain this installation pace over the next seven years.

Solar in Germany: concentration and performance

One notable aspect to understand is the high level of concentration in countries located far from the equator. As shown below, the differences between May 2024 and December 2023 are drastic.

For example, the absolute generation record was broken on 14 May 2024, with a peak of 47 GW2.

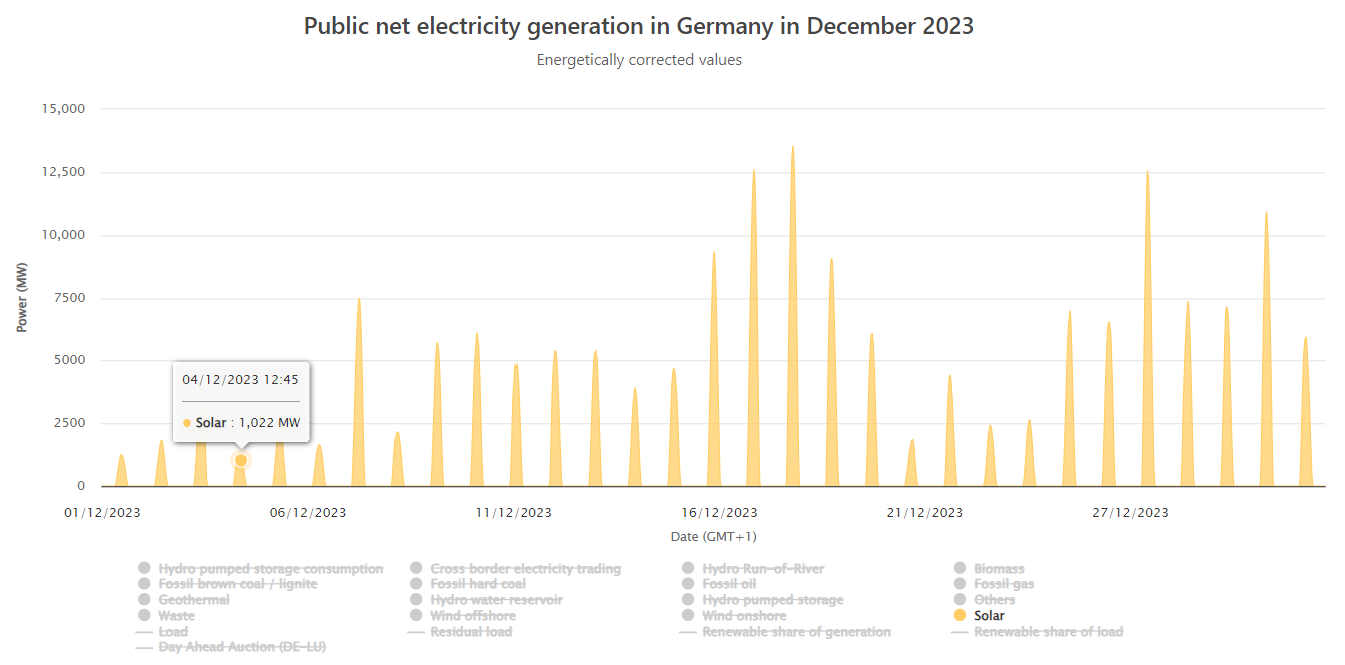

Examining December 2023, the disparity is striking. Solar generation peaked at only 13 GW for the entire month, with some days seeing peaks of merely 1 GW.

When examining the total energy produced per month, we observe a tenfold difference between the best-performing and worst-performing months. This significant seasonal variation poses the main challenge for large-scale solar integration into energy systems at German latitudes, especially with the electrification of heating. This is why the impact of solar will be very limited in the winter months, while it will become preponderant in spring and summer. As mentioned in a previous post, economical seasonal storage solutions are currently unavailable, except in a few countries that can store substantial amounts of energy in their water reservoirs.

The graph below shows the monthly solar generation in Germany since 2020.

In addition to the seasonal effects, daily fluctuations also contribute to a highly concentrated distribution of solar energy production in Germany, as depicted in the graph below. Each band represents 5% of the total hours in a year. Notably, 26% of all solar energy produced in 2023 was concentrated within just 5% of the time. Furthermore, 46% of the production occurred within 10% of the time, and 62% within 15% of the time.

This concentration presents significant management challenges, as solar energy has a substantial impact during these peak hours but a minimal impact during the remaining 85% of the time. Increasing grid flexibility through enhanced storage solutions, dynamic pricing, and the integration of electric vehicles can help mitigate these challenges. Additionally, proper incentives can encourage a reduction in solar yield during peak hours and an increase during off-peak times, such as the use of vertical solar installations3.

The rise of negative prices

Unsurprisingly, negative prices have been on the rise in 2024. The graph below shows the cumulative number of negative prices in Germany's day-ahead market. Aside from 2020, which was marked by the unprecedented COVID-19 situation, 2024 is experiencing a higher number of negative prices.

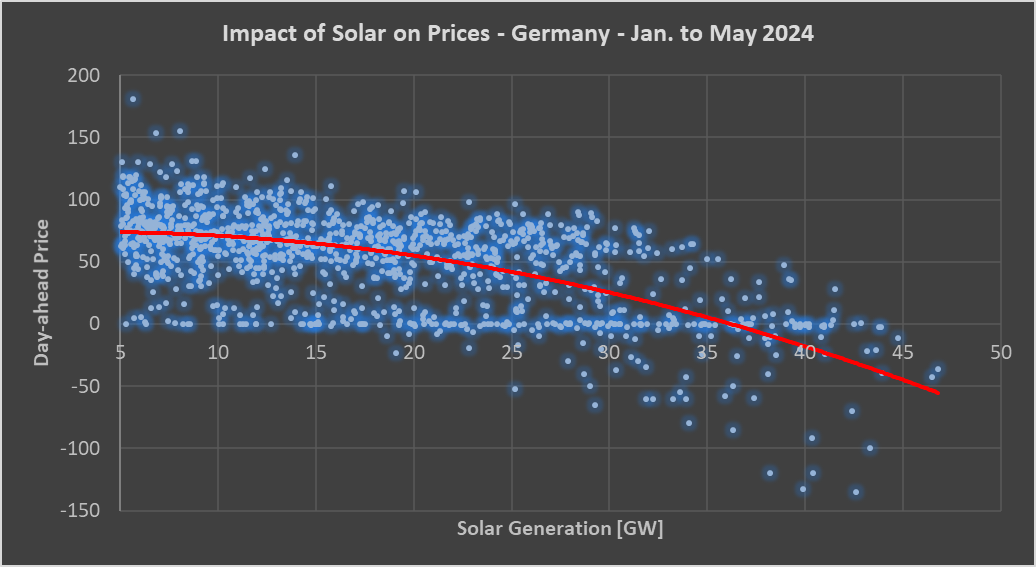

Examining 2024 more closely, the scatter plot below illustrates the impact of solar generation on day-ahead prices. The x-axis represents hourly solar generation, while the y-axis shows the day-ahead price. Each point corresponds to one hour. The plot clearly demonstrates a decline in prices as solar generation increases. Notably, significant negative prices (e.g., below -50 €/MWh) occur exclusively during periods of high solar generation.

Upon closer examination of the bids, a robust correlation emerges between must-sell bids (represented in black) and solar generation (depicted in yellow), as illustrated below. The graph below is from a must-watch webinar on negative prices in Europe.

This bidding behavior prompts solar generators to continue production even when market prices plummet into highly negative territory. While it might seem counterintuitive, it's a direct consequence of economic incentives. In various European countries, including Germany, a significant portion of solar capacity lacks the incentive to halt production during periods of negative market prices. In Germany, two main categories of solar energy are supported by the state: rooftop solar and large-scale solar installations4.

Incentives for large-scale solar are moving in the right direction, with plans to gradually phase out support in the event of negative prices.5. However, for rooftop solar, feed-in tariffs will continue to apply regardless of market prices. Presently, rooftop solar comprises about two-thirds of all solar capacity. Over the next five years, from 2024 to 2028, it is anticipated that approximately 90 GW of solar capacity will be added, with half of it coming from rooftop installations6. Practically, with nearly 10 GW of inflexible solar being added each year, it's inevitable that market prices will be pushed into more frequent and severe negative territory, as flexibility solutions are currently not being deployed at the same pace7.

Solar capture rates are plunging

Logically, the capture rate of solar is therefore dropping fast. In May 2024, it was only about half, meaning that the average solar producer would only capture half of the average market price in May. This drop in capture rate would have to be compensated by the one taking the price risk, in case it drops below the breakeven price of solar projects. For solar in Germany, the price risk is often taken by the German State as the majority of new solar capacity will come from the governmental auctions for large-scale solar and the feed-in tariffs for rooftop solar8. In addition, since the energy crisis, this support is now funded via the German federal budget and is no longer included in the electricity tariffs9.

By looking at the shape of the curves in May, we can clearly understand why the solar capture rate has dropped significantly. The graph below presents the average day-ahead market prices for May in 5 European countries. Looking at Germany, we can observe that some afternoon hours were on average below 20 €/MWh, while the peak hour was above 120 €/MWh. A modified curve has been added for Germany, representing the average day-ahead price in case negative hours were set to 0 €/MWh instead, showcasing the impact of large negative prices on the shape of the curve.

And solar is impacting power reserves

The impact of solar is not limited to day-ahead market prices but goes into every aspect of the electricity markets, including the market for power reserves10. In Germany, the three types of power reserves (FCR, aFRR, and mFRR) are all procured daily on blocks of 4 hours11. The graph below displays the capacity prices of power reserves for each block in May, alongside the average residual load (left side). Highlighted in blue, it is evident that capacity prices, particularly for downward regulation, tend to increase significantly when the residual load is very low.

The logic is relatively straightforward: with fewer conventional generators operating, there are fewer providers of power reserves, driving up prices. Additionally, some generators remain online even when wholesale prices are low or negative, compensating for their revenue shortfall by offering power reserves at higher prices.

Depending on the block considered, the total cost of power reserve capacity is becoming increasingly significant. Below is the sum of the capacity price for all reserves, expressed in € per MWh of load. This metric indicates the amount paid for each MWh consumed in Germany to ensure sufficient power reserves for safe grid operations. As illustrated, this value varies considerably, ranging from 0.5 €/MWh during the night block (midnight to 4 AM) to 8 €/MWh on May 13th between 8 AM and noon. Furthermore, the most expensive periods are the morning and afternoon blocks, with costs of 2.2 €/MWh from 8 AM to noon and 2.4 €/MWh from noon to 4 PM.

This also underscores the increasing need for enhanced flexibility solutions to manage periods when conventional generators are not available.

In conclusion

The evolution of our electricity grids is a fascinating story. One major transformation underway is the rapid increase in solar capacity, especially in Europe and Germany. Here are some key points:

In German latitudes, solar is very concentrated for a relatively limited number of hours. 62% of the solar energy produced was done on only 15% of the hours. In more Southern latitudes, like Spain, this concentration is much less pronounced.

This concentration means that the impact of solar in winter is negligible. Starting in March/April, we start to experience an important impact of solar, where duck curves would become the norm.

Solar capture rates are declining fast in such a context. With the planned increase in solar capacity, it is unlikely that the trend will reverse.

Support for solar will become slightly more expensive as the capture rates decline. It is unclear if the cost reduction in projects would be sufficient to compensate for the decreasing capture rate. If not, sufficient financial support would be needed to keep the momentum.

Flexibility (such as batteries, demand-side management, electric vehicles, dynamic prices, etc.) will be key. Nevertheless, we should not only foster flexibility but also try to remove the sources of inflexibility. Concretely, we should remove support schemes that incentivize people to generate irrespective of market prices, as it is a key driver for large negative prices. This would mean for example introducing market-based components into support schemes for low-voltage installations.

Every aspect of the market is impacted, including power reserves. We are observing a correlation between solar generation and the prices of power reserves. It is likely though that the development of flexibility assets, and in particular storage, would bring innovative solutions for increasing system flexibility and power reserves in particular.

Thanks for reading.

Interestingly, they are paid at a much higher price (above 200 €/MWh) on average than new solar installations. See the calculations here (slide 6).

Even though data quality might be an issue, it should be noted that it is quite low compared to the installed power of 87 GW.

See my previous post on vertical solar.

Called Solare Strahlungsenergie aus sonstigen Anlagen and Solare Strahlungsenergie aus Freiflächenanlagen respectively.

See the EEG 2023, paragraph 51: payments are stopped in case of negative prices for at least 4 hours in 2023. In 2024 and 2025, payments are stopped for at least 3 hours, in 2026, for a least 2 hours and finally, in 2027, for one hour only.

This could be reversed of course in the mid to long-term, depending on a broad range of factors making long-term projections (beyond 5 years) extremely challenging.

Some new solar is unsupported in the form of commercial PPA for example. The first quarter of 2024 has seen 648 MW of new PPA in Germany, for wind and solar combined (source).

There are 5 auctions, two different ones for aFRR and mFRR for upward and downward directions.

Viewpoint from German home owner.

I moved to Germany in 2011 from Austria. Bought a duplex with a small roof. I was immediately confronted with almost double electric rates compared to Austria. Reason being I was forced to subsidize my neighbors solar installation. I said if you can’t beat em, join em. Installed a modest 3Kw Rooftop system. It was artificially throttled back to 2.5 Kw. Then one could install extra equipment to allow the utility to shut down your system during peak hours or take a 30% reduction off the top. This reduction was recently removed for new installs just last year.

In any event I receive 16 cents for my excess solar production. Early installations received over 50 cents. My income is about €250 a year. With ever increasing electric rates I invested further. I added 4 more modules on my carport ( shaded in winter) and an additional 3Kw inverter (Bluetti) and 6 kWh batteries. Later another 3 KWh battery and 5 Kw inverter to handle typical house loads. Recent changes in law removed the VAT (19%) on anything solar.

So now in June I am 72% self sufficient and use 55% of my solar. Grid feedback is actually reduced due to battery installation and what I purchased also decreased. I run my refrigerators, washing machine and heat water for kitchen all from solar.

In June. NOT in November to March. In winter I depend 95% on the grid.

On top of this there was no thought or consideration of the batteries in the EV’s being used for the house until just recently. V2G. Vehicle to Grid. In Asia being done for years. German electric cars not capable. No well thought out economical and scientific feasible plan. Just put wind turbines where there is no grid and millions of mini generators on a grid not designed to support it.

During this time period Germany shut down all of its clean and paid for Nuclear generators. And keeps paying the Nuclear generator owners for what they didn’t earn. And pays the home owners for the electricity they cannot use and have to pay to dump. And enjoys one of the highest electricity rates in the world.

You can’t make this stuff up.

What is the point of spending billions on RE when it fails on nights with little or no wind?

We just get more costly and less reliable energy with massive damage to the planet.

The German trifecta of failure.

You have to import power and deindustrialise.