On Imbalance Prices

With a comparison of Germany and Belgium.

The imbalance price plays an important role in the European power market. It is the tariff applied every 15 minutes to a Balance Responsible Party’s (BRP’s) deviations—whether the BRP falls short of its scheduled position (negative imbalance) or exceeds it (positive imbalance). Since it is impossible to forecast production and consumption perfectly in advance, the imbalance price serves as the mechanism for settling these real-time deviations and ensuring that each BRP’s position is reconciled.

In this post, I will unpack some principles behind imbalance prices and highlighting how they are calculated in Germany and Belgium. Although many of these mechanisms share common roots, practices are far from harmonized.

Why do we need an imbalance price? What’s the objective of the imbalance price?

In simple terms, the imbalance price is the financial bridge between the planned energy market and the physical reality of the power grid. Practically speaking, the imbalance price is designed to be a corrective signal. It must be expensive enough that market participants prefer to balance themselves rather than rely on the TSO.

Now, let’s consider three different situations and check how the imbalance price can actually influence the market actor behaviors.

First, let’s consider that the imbalance price is set at the Day-Ahead market price. In such case, the financial incentive for a BRP to maintain a balanced portfolio effectively disappears. In this scenario, the power grid is treated like a risk-free storage unit. Because there is no penalty for deviating from a schedule, market participants have little reason to invest in forecasting tools or flexible assets. This leads to “moral hazard,” where BRPs allow their imbalances to grow. Ultimately, the actual costs of balancing the system are not reflected in the price, leading to a loss of market efficiency and increased socialized costs for the end consumer.

Secondly, let’s now consider that the imbalance price is set at a very punitive level. In such as case, it creates a climate of extreme risk aversion that can distort market behavior. BRPs, fearing astronomical penalties, will likely “over-hedge” their positions or procure excessive reserves to ensure they never fall short. While this might seem beneficial for grid security, it drives up operational costs significantly. These high risk premiums are eventually passed down to consumers, making electricity unnecessarily expensive. Furthermore, a hyper-punitive environment can reduce competition by creating a high barrier to entry for smaller players or renewable energy companies that naturally face higher volatility in their production schedules.

Thirdly, we consider an imbalance price that is advantageous in only one direction—for instance, being cheap when a BRP is short. In such as case, the imbalance price triggers strategic gaming of the system. If the cost of being short is lower than the price of buying energy on the spot market, BRPs will intentionally under-buy energy to capitalize on the price difference. This creates an asymmetric incentive where participants prioritize their own profit over the physical stability of the grid.

These examples illustrate how the imbalance price can shape market behavior. Ultimately, it comes down to striking the right balance between competing trade-offs in order to create effective incentives.

Single or dual price?

In general, a balancing market can operate under either a single‑price system or a dual‑price system. Under a single‑price system, the imbalance price is the same whether the BRP has a negative imbalance (i.e., it is short and needs energy, resulting in a payment from the BRP to the TSO) or a positive imbalance (i.e., it has a surplus of energy, resulting in a payment from the TSO to the BRP).

Countries typically fall into one of three categories:

Single‑price systems,

Full dual‑price systems,

Hybrid systems, where the market switches between single and dual pricing depending on system conditions, such as the Netherlands.

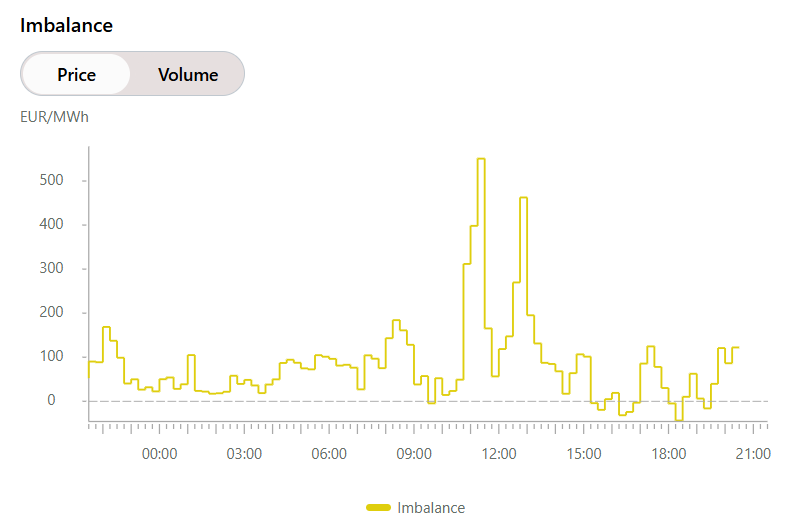

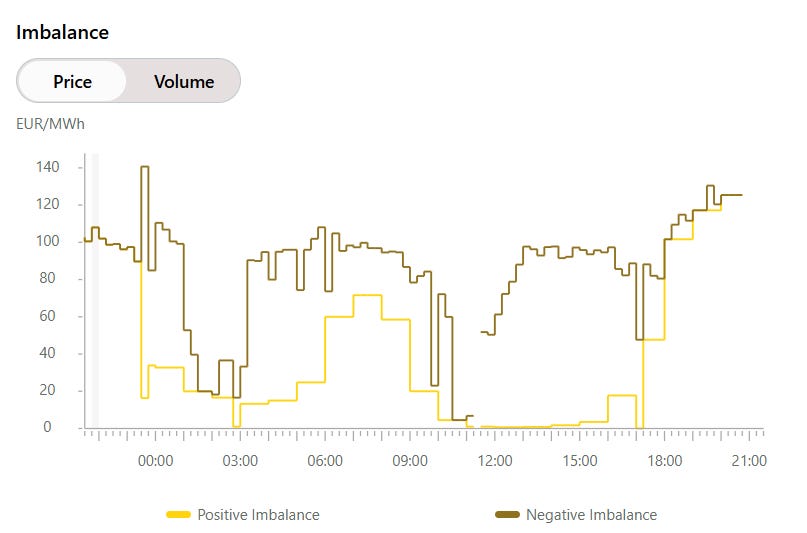

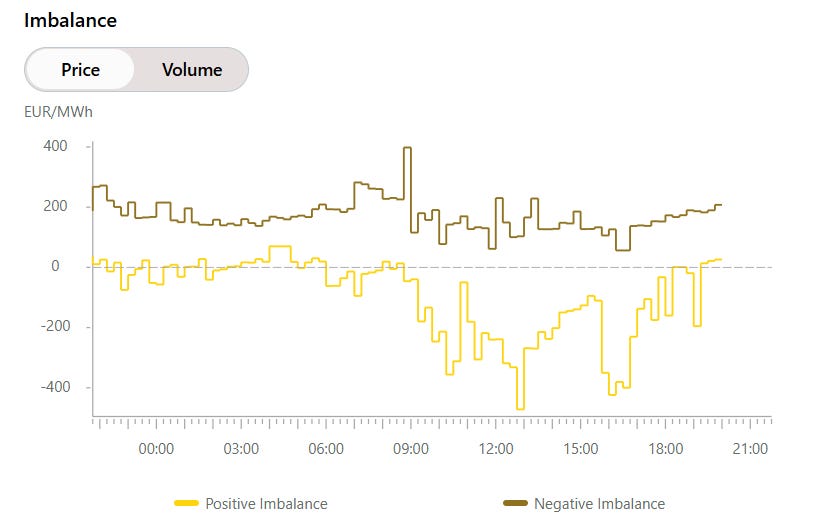

For example, here below, you can see the evolution of the imbalance prices for a day in several countries: Germany, Spain, and Switzerland (before 2026)1.

Single-price

Dual-price

Interestingly, for BRPs, the difference between the two pricing systems is significant. The wider the gap between the two imbalance prices, the more potentially punitive the system becomes. Consider the Swiss example shown above: for most of the daytime period (roughly 9 AM to 6 PM), the positive imbalance price was negative, while the negative imbalance price hovered around 150 €/MWh. In practice, this means:

A BRP with a positive imbalance (surplus) would have received a negative amount—in other words, it would pay the TSO for injecting extra energy into the system.

A BRP with a negative imbalance (shortage) would also pay the TSO to cover its missing energy.

Such a price difference for positive and negative imbalance prices incentivizes the creation of larger BRPs or portfolios: two small BRPs with opposite imbalance positions would benefit by netting their imbalances internally and avoiding these penalties. This portfolio effect largely disappears in a single‑price system, where positive and negative imbalances are valued equally.

The various elements that might exist

As mentioned above, the imbalance price should incentivize the BRP to act to restore their imbalance (and in some countries2, go even beyond, and create an opposite imbalance if it can help the system). Therefore, in general, there is a connection between the balancing energy prices (the prices that TSO pay to activate and restore the balance) and the imbalance price. Nevertheless, this is only a general principle and in practice, we have as many declinations as there are countries in Europe. The principal questions are:

Balancing activation prices: Is the imbalance price directly linked to the prices of activated bids? And if yes, how do we consider them (average, weighted average, marginal)? Are both upward and downward activation prices included, or only the marginal activation in the direction of system need?

Scarcity pricing: Are there uplift components that increase the imbalance price when the system is tight?

Is there a dual‑price or single‑price framework? Are positive and negative imbalances settled at the same price or at two different prices ?

Cross-border effect: In countries participating in international balancing platforms (MARI, PICASSO), do foreign activations influence the domestic imbalance price?

Volume-based component: Does the magnitude of system imbalance influence the price (e.g., non-linear ramps, penalties, or volume thresholds)?

Intraday price: is there a link with the intraday market?

After the paywall, I will go into more details about the German and Belgian imbalance prices, especially how they are calculated and how they compared to day-ahead prices in 2025.