Renewables need intraday markets

A short presentation of why intraday markets are important for solar and wind

As everyone knows, forecasting the weather, and consequently renewable energy output, is prone to errors, especially the further in advance it is done. Beyond trends associated with seasonal patterns, accurately predicting wind and solar generation weeks in advance is impossible. Because consumption must match generation in real-time, there is a crucial need for mechanisms to continually adapt previous forecasts and therefore, market positions until delivery. This is where intraday markets play a crucial role.

Let's explore why these intraday markets are essential and what could happen in their absence.

Renewables cannot be predicted perfectly

Wind and solar, the primary drivers of increasing renewable energy penetration, depend highly on weather conditions. Unfortunately, predicting wind and solar output with precision is challenging, particularly as the forecasting horizon extends further into the future.

Here is an example comparing the day-ahead forecast, the most recent forecast1, and the actual generation. As we can see, the differences between the three can be substantial, with actual generation exceeding the day-ahead forecast by more than double at certain times.

Of course, forecasts are not always inaccurate. On clear blue skies or uniformly cloudy days, solar generation is easier to predict. The most challenging days are those with partial cloud cover, as accurately predicting the precise location of clouds is difficult. Below is a comparison between the day-ahead forecast and the actual generation for Germany in 2024, demonstrating that substantial deviations are not very frequent.

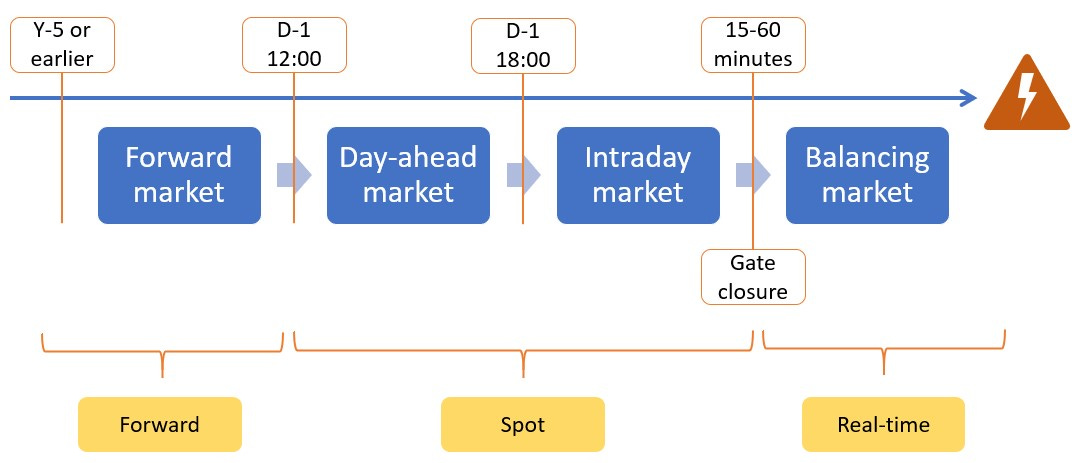

The European power markets: a timeline

The European power markets are structured according to the following timescale (in addition to the spatial distribution)2.

Forward market. Either over-the-counter or organized markets3, these markets generally serve as hedging instruments against the inherent volatility of the spot market. Market players use them to ensure price stability over a long period. These markets can settle electricity trades from several years in advance to a few days before delivery.

Spot markets:

Day-ahead markets. Often considered the cornerstone of European power markets, buyers and sellers submit bids for the following day before noon4. Prices per hour and bidding zone are established for the 24 hours of the next day.

Intraday markets:

Auctions. At regular intervals5, auctions are organized following a similar principle to the day-ahead markets.

Continuous. This is the main tool for trading after the gate closure time of the day-ahead market. Trades between sellers and buyers can be settled continuously (unlike the single price of intraday auctions and day-ahead markets) until 15 to 60 minutes before delivery, depending on the country.

Balancing market. At a specific time before delivery6, the Transmission System Operator (TSO) takes over the responsibility to balance the system. This is achieved through various products (such as FCR and aFRR, as mentioned in my previous posts) or through implicit reactions from market parties based on the imbalance price7.

Renewables need intraday markets

The need to have short-term markets due to our impossibility to predict precisely the renewables output has been recognized at the highest European level, as we can read in this letter from the EU General Secretariat of the Council:

Intraday markets are particularly important for the integration of variable renewable energy sources in the electricity system at the least cost as they give the possibility to market participants to trade shortages or surplus of electricity closer to the time of delivery. Since variable renewable energy generators are only able to accurately estimate their production close to the delivery time, it is crucial for them to have a maximum of trading opportunities via access to a liquid market as close as possible to the time of delivery of the electricity.

This recognition is logical, as it becomes clear that day-ahead markets alone are insufficient for managing renewables. With the gate closure time set at noon the day before, the renewable output must be predicted up to 36 hours in advance, something that will never happen without errors.

What happens in case of a large deviation?

Let’s consider the 3rd of June. At 10 AM, the day-ahead price in Germany was 99 €/MWh, a relatively typical situation. However, the intraday markets showed the following prices:

To clarify:

The highest price recorded at 10 AM was 9122 €/MWh, which is 92 times higher than the day-ahead price.

The average price in the intraday continuous market was 766 €/MWh.

The ID-3 average, the weighted average price of all continuous trades executed within the last three trading hours8, was close to the continuous average at 782 €/MWh.

The ID-1 average, the weighted average price of all continuous trades executed within the last trading hour, was 2519 €/MWh.

It is evident that as we approached real-time, the market increasingly noticed a power deficit, making it more challenging to close the gap, resulting in higher prices.

As previously mentioned, at a certain point, the transmission system operator (TSO) takes precedence over the spot markets. Any deviation between generation and consumption within a Balancing Responsible Party9 will be billed at the imbalance price. Here is the imbalance price on 3 June, where we can see that the imbalance price was very high (peaking at 14978 €/MWh at 9 AM) from 8 AM to 10:30 AM.

So, what could have caused this situation? It was likely a combination of factors, and I cannot identify all of them. However, one contributing factor was the forecasting error for solar production. At 10 AM, solar production was 12.8 GW, which was nearly 4 GW less than what was expected just 2 hours earlier and almost 7 GW less than what was forecasted in the day-ahead forecast at 6 PM, as shown in the table below.

As market participants aimed to avoid the punitive imbalance price, intraday markets started trading at higher prices, which continued to climb as real-time approached. Without the availability of intraday markets, the corrective actions that the TSO would have needed to take in real time would have been much more significant. Therefore, intraday markets are extremely valuable in reducing the "balancing burden", especially as we incorporate more weather-dependent generation sources. Nevertheless, it should also be noted that large traditional plants and interconnectors also add unpredictability due to potential unplanned outages leadng to sharp imbalances.

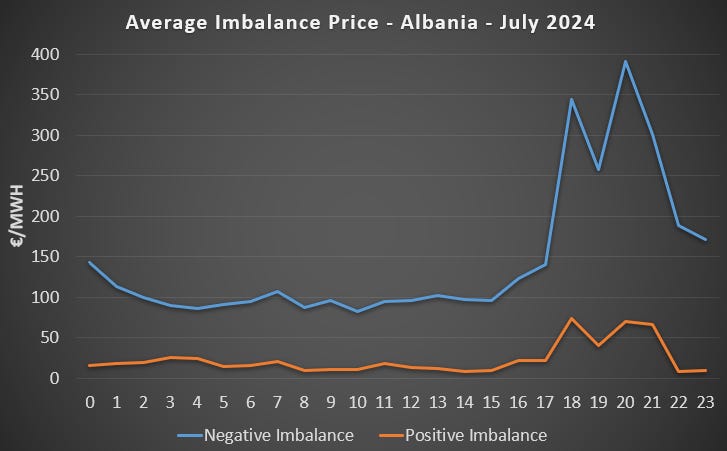

What happens without short-term markets: the Albanian case?

Unfortunately, not all countries have liquid intraday markets and one example is Albania. The country is in the process of integrating its energy markets into the European ones. Several steps have been taken, including the creation of a balancing market in 2021 and the launch of a day-ahead market in 2023, which has since been coupled with Kosovo. However, the country still lacks an intraday market, and the overall liquidity of all its markets remains low.

As a result, renewable energy producers in Albania, who are now generally obligated to manage their own imbalances, face significant challenges without intraday markets. Let's examine the consequences for renewables such as wind and solar under different scenarios:

Supported by Feed-in Tariffs (pay-as-produced): In this case, the producer does not pay any imbalance price, as they receive a fixed remuneration for actual generation. The imbalance risk is effectively transferred to the buyer.

Supported by a Contract-for-Differences (pay-as-nominated): The producer must sell their generation on the day-ahead market. Any difference between the day-ahead forecast and actual generation must be paid for by the producer at the imbalance price. In Albania, a dual pricing system exists, with different prices for negative and positive imbalances.

Not Supported by a Governmental Agreement: Similar to the second case, the producer must bear the cost of any imbalance at the corresponding imbalance price.

Below is the average imbalance price per hour in Albania for July 2024. This illustrates the potential financial impact on renewable producers who cannot correct their forecasts through intraday trading.

Practically in July 2024, the negative imbalance price was around 100 €/MWh while the positive imbalance price was typically around 20 €/MWh. This means that if a producer overestimates their production, they will have to pay the TSO the negative imbalance price. Conversely, if the producer generates more than predicted, they will only receive the positive imbalance price.

This creates a significant financial risk10, as forecast errors over 24 hours or more can be substantial, especially for specific locations11. To mitigate this risk, recent large solar and wind auctions in Albania have maintained a pay-as-produced system. A pay-as-nominated system will be introduced once the market is sufficiently liquid, but with a cap on the maximum amount (which must be financed by someone). While this cap provides producers with protection against high balancing costs, one could also argue that it diminishes the incentive for accurate forecasting.

In conclusion

Forecasting renewable energy production will never be completely accurate, and prediction errors are inevitable. This underscores the need for short-term markets, such as intraday markets, to help balance supply and demand closer to real-time. Moreover, the liquidity of these markets is crucial to ensure that buyers and sellers can consistently match their trades. Therefore, market coupling of power markets, including intraday markets, is vital for the development of renewable energy, especially for smaller countries like Albania.

Updated every hour.

Electricity is about timing and location.

Some countries have slightly different gate closure times.

There are in continental Europe, three Intraday Auctions.

This is not the same for all European countries but it is generally between 15 to 60 minutes.

Not allowed in all countries.

This dual imbalance pricing system poses a significant financial risk. However, even in a single imbalance price system, the producer is generally at a disadvantage. Since imbalance prices are often correlated with weather forecast errors, producers usually face higher costs when they fall short of their forecasts. When the system is short and imbalance prices are high, producers typically experience shortfalls themselves, leading to substantial financial penalties.

A single location is much more prone to deviations than a larger geographical zone, such as a whole country, as shown in the examples above.

An interesting article. However, it suffers from circular logic. Fact: renewable output has significant error bars when looking 24hrs ahead. Assertion: intraday markets are important for RES integration into the elec system. Fact: many (most?) renewable projects are being connected under CfDs – which insulates a given RES project under CfDs from market wobbles. Why then are intraday markets helpful? The problem is as follows: the elec system needs determinism to operate in a stable fashion (balance load and generation – from real time through to multi-day). Determinism has declined (fossil exiting/de-carb) and what is left can be costly. As I have repeatedly noted, no serious effort has been made to address the storage problem (where to put the surplus elec) and the obverse – what happens when no-wind and no sun. Demand response? The EU has been talking about it for north of a decade – little real action (generators don’t like it amongst other reasons). The article claims that markets can help balance – but that claim rests on pricing – the pricing of MWh to force balance. But if you have a CfD why would you be worried? As for the massive price oscillations – looks like bank prop-desks trying to make a killing – we know they are plays in this game – you only need to look at the 4:1 ration – elec trading vs delivery. This is not markets delivering sensible prices, this is a casino & the ones who ultimately pay are Euro serfs.

renewables need batteries and a regime that involves them as a central market, - intraday markets are to an extent, a distraction from the most important change that we need to support renewables. We need to create specific markets for batteries, not a second market compared to contracts for energy supply. You often talk about how to increase the market value of solar pv. Building a regime that more encourages batteries will do that much better than altering contracts for solar pv which may restrict their growth