Solar (and wind) for power reserves

Why renewables, especially solar, should provide power reserves: key reasons and business opportunities

Power reserves, or ancillary services, play a crucial but often overlooked role in our power sector. While they might be familiar mainly to industry professionals, they are vital for the safe and reliable operation of our power grids. Historically, renewable energy sources have not been significant contributors to power reserves. However, as the share of renewables like wind and solar increases, it's becoming increasingly important for these sources to also provide power reserves.

In this post, I will explore why it is both timely and feasible to start integrating power reserves into solar power systems, particularly for large-scale solar farms.

The declining market value of solar

As I have discussed in previous posts, the market value of solar energy has been steadily declining. The tables below illustrate this trend by showing the solar capture price (first table), the average market price (second table), and the solar capture rate (last table) for five European countries. The data reveals that some countries have faced significantly low solar capture prices recently. For instance, in April, Spain's solar capture price was just €6/MWh, France's was €14/MWh in May, and Germany's has been below €40/MWh for several months.

Given these capture prices, can solar explore alternative strategies to increase revenue?

Additional revenues

Traditional power plants often generate additional revenue by providing power reserves. Despite ongoing efforts to standardize power reserve systems across Europe, significant differences remain between countries, making it challenging to draw broad conclusions, especially concerning remuneration and business cases.

Typically, entities that provide power reserves are compensated for the service they offer to the grid. This service is in general the ability to regulate downward or upward the power output to maintain the overall system balance1. In Europe, power reserve services are categorized into various products, each with distinct characteristics2.

Historically, renewables like wind and solar have not participated in providing power reserves. This is largely because their marginal cost is zero, leading to a focus on maximizing total generation rather than providing reserve capacity. Support schemes have traditionally prioritized increased production, leaving little room for power reserves. However, as the share of wind and solar energy grows, it becomes evident that focusing solely on maximizing production is no longer sufficient. The emphasis should shift toward maximizing overall value.

Since value is derived not just from energy markets (such as day-ahead, intraday, or long-term markets) but also from participating in power reserve markets, renewables should engage in these services to generate additional revenue, much like traditional power plants. Additionally, incorporating renewables into power reserves could lessen the dependency on fossil fuel plants solely dedicated to providing reserve capacity.

This is already the case in some markets

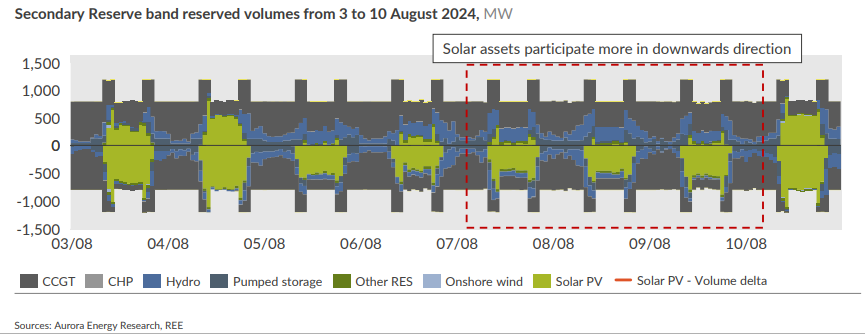

Let’s be clear: what I suggest here is already done. Here we can see that solar PV is already participating massively in the secondary reserve in Spain, both for downward regulation (lowering generation) and for upward regulation, even though for upward regulation, it is mostly on specific days, when the day-ahead prices were low or even negative.

In other regions such as Belgium and Germany, wind already provides reserves, especially in the case of downward regulation.

Business case 1: downward flex

A straightforward opportunity for solar is to engage in downward regulation services, such as aFRR3, similar to practices in Spain. In Belgium and Germany, aFRR is procured in 4-hour blocks each day, split into downward and upward regulation. Analysis of pricing trends shows a significant increase for the afternoon block (12 to 16 hours).

The unit is €/MW per hour, indicating the remuneration the asset receives for each MW of downward flexibility provided. In July 2024, the monthly average price for the 12 to 16-hour block exceeded €40/MW per hour, highlighting a substantial revenue opportunity for providing downward flexibility

In Belgium, a similar, and perhaps even more pronounced, trend can be observed. For example, on Sunday, August 11, 2024, the average and marginal prices for aFRR are plotted below. It’s important to note that aFRR capacity pricing operates on a pay-as-bid basis rather than a pay-as-clear model.

The data reveals that “sunny blocks” experience exceptionally high prices, with some exceeding €350/MW per hour. Practically, this means that if you have 1 MW of flexible generation, you can still generate energy on the day-ahead market (where the average price is around €50 to €100/MWh, though it was negative on that particular sunny Sunday). Despite the low or negative energy price, you could earn significantly more for simply providing flexible capacity.

Remuneration for aFRR services includes both capacity prices and activation prices. Often, activation prices for aFRR downward can turn negative relatively quickly. Grid operators prioritize activating the least expensive aFRR downward services, which corresponds to the highest bid prices, since payment flows from the grid operator to the provider.

Every 15 minutes, bids are ranked in a merit order. The graph below illustrates this merit order for two specific intervals on August 22, 2024, in Germany: from 00:00 to 00:15 and from 12:00 to 12:15. The data shows that during a significant portion of aFRR activations, the activation prices are quite low, especially falling below -€200/MWh during midday. Additionally, it's important to note that this market is capped at ±€15,000/MWh in Germany.

To achieve flexibility with solar power, it's crucial to ensure the availability of generation capacity. For large-scale solar plants, it is often possible to forecast generation levels with a reasonable degree of accuracy. Based on these forecasts, a plant can confidently offer a portion of its output as downward flexibility.

For example, consider a solar farm in Spain. Over the course of the week of 15 to 21 July, except for July 18th, the plant consistently generated enough power that it could have offered a significant share of its output as downward regulation.

Of course, Spain is more conducive than Germany for downward regulation as the capacity is procured on an hourly level. The 4-hour blocks in Germany and Belgium might represent a barrier, even though it is not clear to which extent4.

Providing flexibility is certainly easier with large solar parks, like those in Spain, compared to distributed solar installations, which are more common in Belgium and Germany. However, it should be technically feasible to aggregate smaller solar installations and offer flexibility services as a collective group.

Business case 2: upward flex

This scenario is similar to the previous one, but here, upward flexibility is offered, meaning the ability to increase generation. Achieving this requires consistently operating below maximum capacity to maintain an upward reserve. While it may seem counterintuitive to curtail zero-cost energy production, this approach makes sense given the declining value of electricity prices when renewable output is high. Below is an example showing the evolution of normalized prices in the Netherlands during the sunny months (April to July). It is evident that the value during afternoon hours is dropping significantly.

Therefore, if support schemes don't interfere with proper market incentives (which I’ll discuss later in the post), a viable business case could emerge for proactively reducing solar generation to create an upward flexibility reserve. In fact, if market prices fall below a certain threshold (perhaps 5/10/15 €/MWh), there could be a strong incentive to curtail production and instead offer capacity as upward flexibility in markets like aFRR or other flexibility services. Interestingly, this approach could result in the marginal cost of solar bids in the day-ahead market being higher than zero, as it opens up opportunities for additional revenue streams5. This bidding behavior at a price higher than zero could also be influenced by factors such as opportunities in imbalance prices (discussed below) or other short-term market dynamics.

The main rationale is that as day-ahead prices approach zero or turn negative during sunny periods, solar generators have a clear opportunity to reduce output—since the value of generation is minimal or even negative—and offer upward flexibility to the market. This approach could be combined with providing downward flexibility, as mentioned earlier.

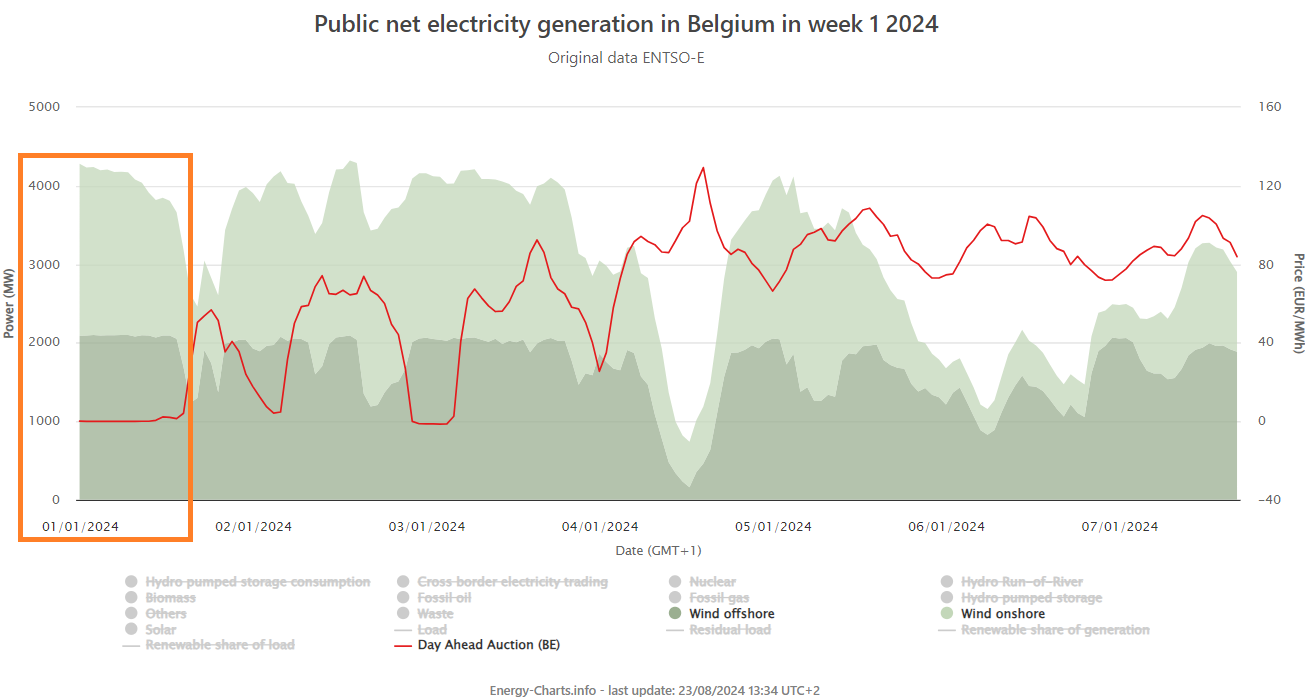

This concept can also apply to wind energy. For instance, on January 1, 2024, strong wind production drove day-ahead market prices to zero throughout the morning (as shown by the red line below). Meanwhile, Belgian aFRR upward capacity prices averaged 82 €/MWh for the time blocks between midnight and 8 a.m. In this scenario, reserving a portion of power for upward flexibility proved to be a viable market strategy.

Business case 3: imbalance prices in Belgium

In this section, I will explain the specifics of a unique market: the imbalance market in Belgium. Each country has its own rules for managing imbalances—the differences between generation and consumption within the portfolios of market parties6. For each imbalance, market participants either pay the grid operator if they are short (lacking generation) or receive payment from the grid operator if they are long (excess generation). The amount paid or received is determined by the imbalance price.

In Germany, it is legally prohibited to intentionally create imbalances to profit from these prices, whereas, in Belgium and the Netherlands, this practice is allowed. The challenge, however, lies in the fact that the final imbalance price is typically known only after the considered period (ex-post), which introduces the risk of being on the wrong side of a trade7. Despite this, the volatility of imbalance prices in Belgium can make the market attractive. In the Netherlands, the situation is even more complex due to the potential for dual pricing8.

To illustrate the increased volatility, the following graphs highlight the rise in negative imbalance prices. The first graph shows that when the imbalance price is negative, it has become increasingly more so. The second graph indicates that the share of time when the imbalance price is negative has also risen, reaching nearly 40% in January and April 2024. Finally, the last graph combines these effects, presenting the monthly cumulative value of the imbalance price when it is negative.

Similar to downward flexibility, solar installations could be incentivized to reduce production when negative imbalance prices are available.

Additionally, a similar approach could be applied to upward regulation. For instance, on July 21, 2024, the imbalance price exceeded 150 €/MWh for most of the hours when solar was generating, while day-ahead market prices were at zero from 9 AM to 4 PM. In such cases, a solar plant that reacts solely to market prices might find a viable business case in reducing production to reserve upward flexibility and capitalize on positive imbalance prices.

Competition with storage

As solar and wind energy come to dominate the generation mix, the role of traditional power plants in providing flexibility diminishes. One rapidly growing solution to this challenge is energy storage. It is likely that an increasing share of power reserves will be supplied by storage facilities.

However, as day-ahead market prices plummet during peak solar generation, it becomes increasingly advantageous for solar installations to shift towards offering power reserves. While it’s difficult to predict which technology will dominate reserve provision in the future, it will likely involve a combination of various grid assets, with the optimal solution varying based on real-time grid conditions. Business cases for batteries are relatively good9 with current prices for reserves and flexibility in general but increased competition from batteries as well as renewables might lower the remuneration for flexibility in the mid-term.

Being smart with support schemes

To conclude, it's important to note that support schemes for renewables can significantly limit the business case for providing reserves with solar and other renewable sources. Many support schemes, particularly for solar, prioritize maximizing production without considering market and grid conditions. This approach does not support the flexibility that could be provided by solar.

Ideally, support schemes should not decrease market incentives, including day-ahead, intraday, power reserves, and imbalance markets. More effective schemes, such as financial Contracts for Difference (CfD) or capability-based CfD, should be preferred over traditional CfD or Feed-in Tariffs, as they better accommodate market dynamics and encourage flexibility.

If you have further questions on the ideas developed in this post, do not hesitate to contact me.

Thanks for reading,

Julien.

There are other services such as voltage regulation and black start, but broadly speaking, regulating up and down is the most common regulation support.

Check out my post on aFRR.

For the blocks 4 PM to 8 PM, this is probably impossible as generation close to 8 PM is generally minimal.

To be fair, I got this idea from Benjamin Genêt working at Elia,

Also referred to as Balancing Responsible Party.

Within the period, generally, a quarter-hour, as we are moving towards the end of the period, the certainty of the final imbalance price increases.

See the various posts of Jean-Paul Harreman on that matter.

It looks like offshore wind played business case #1 in July in France: https://www.linkedin.com/posts/galileo-barbieri-7387343_l%C3%A9olien-off-shore-participe-%C3%A0-la-flexibilit%C3%A9-activity-7230209375192166400-UdEg The comments to the LinkedIn post indicate that more explanations are needed…!

Seasonal thermal storage for heating or cooling can create large new markets for solar energy that can reduce the potential for price collapses, while continuing to offer grid services. Underground thermal energy storage can be very low cost.