Will utility-scale batteries reduce volatility in the day-ahead markets?

In short, no. Indeed, it is unlikely that utility-scale batteries will have a meaningful impact on the price volatility in the day-ahead markets for the coming years.

Utility-scale batteries are batteries with an energy content in the tens or hundreds of MWh. As battery cost is dropping, there has been an increased interest in installing these large-scale batteries around the world1. But what could these batteries actually bring to the electricity grid? Specifically, can they reduce the large spread in day-ahead prices, especially when the sun is shining? Let’s dig in.

Volatility on the rise

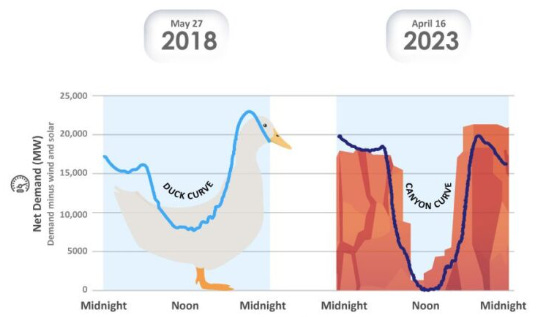

Volatility in the day-ahead markets is set to increase in the coming years, especially during the peak of solar generation, also referred to as the duck curve or even the canyon curve. We discussed this topic here.

During the last week of May, the current solar capacity2 was sufficient for the day-ahead prices to be extremely low and even negative across Europe.

These very low prices can be explained by the share of solar generation as we can see in the graph below depicting the total load (black line) and the residual load or net load (gray line). The net load is the total load minus the generation from wind and solar. We can clearly see that for 25, 26, 27, and 28 May, the German residual load was similar to the “canyon curve”.

As explained in a previous post, we are only at the beginning of the solar revolution. Indeed, solar is expected to increase fast: SolarPower Europe expects that 50 GW of new capacity would be installed in 2023 across the EU and it would increase every year to reach 85 GW in 2026. IEA is forecasting an additional solar capacity of around 90 GW in the coming two years. REPowerEU has the objective to achieve 750 GW by 20303. With the current installed capacity of slightly above 200 GW, we can expect a doubling in capacity within four years. The direct consequence is straightforward: the “canyon curve” is going to be a common feature in the day-ahead markets.

With this observation, is it interesting to install batteries to buy the dip and sell during the evening peak?

Utility-scale batteries: the silver bullet?

Large-scale batteries are sometimes considered a solution for the volatility of the day-ahead markets. In a recent article, an official from the Serbian power exchange explained:

The phenomenon where electricity prices drop to zero and below can be prevented with storage systems such as batteries.

Similarly to the previous quote, and after the same wave of very low prices during the last weekend of May 2023, the Belgian energy minister tweeted:

Battery farms provide flexibility. Store green energy when there is a surplus and return it when there is demand. Thanks to a favorable Belgian investment climate, the largest battery parks in Europe are being built in Belgium. This way we realize lower prices and less CO2.

Let’s start with a simple statement: an increased penetration of renewables means that we will need more flexibility in our grid and large-scale batteries are able to provide flexibility. But what does flexibility mean? Is it allowing the voltage to stay stable? To allow minutes-scale variation of renewables? Or hourly/daily/seasonal? Or it means less congestion in the grid? Flexibility can mean many things.

In this post, we will argue that large-scale batteries are currently effective to provide flexibility in the form of grid services but are still uneconomical to perform energy arbitrage on the day-ahead markets.4 It is therefore unlikely that the fluctuations of prices on the day-ahead markets would be impacted in a meaningful way by large-scale batteries.

Back-of-the-envelope calculation

Let’s do a quick analysis with a large-scale battery bidding on the day-ahead market. Of course, no company will invest only for arbitrage on the day-ahead but at least, such a calculation could provide some insight on the current value of large-scale batteries for arbitrage on the day-ahead market.

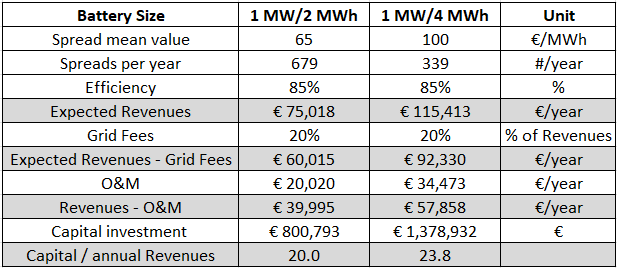

The table below presents the results for two battery sizes: 2-hour storage and 4-hour storage. All the calculation is per MW. Capital costs and O&M are from NREL. We assume that the battery of 2 hours could realize two price spreads per day on average of 65 EUR/MWh and the battery of 4 hours, one spread per day of 100 EUR/MWh. We also assume grid fees of 20% of the revenues and an availability factor of 93%. Of course, we can discuss the assumptions but we believe that they are rather generous for the business case already5.

These expected revenues are unlikely to attract investments in arbitrage in the day-ahead markets. Of course, in exceptional cases, already installed batteries could also be active in the day-ahead markets but it is unlikely that they would be installed primarily for that matter6.

What do others say about the question?

Let’s also review what some other authors are saying on the question.

Dr. Iain Staffell presented an analysis of the most competitive storage technology depending on the number of discharges per year and the duration of the discharge. At current technology costs, pumped hydro is particularly well-placed for the range of interest, compared to batteries.

Thomas Mercier et al. published a paper on the value of electricity storage arbitrage on day-ahead markets across Europe. It appears that for 5-hour storage, the yearly revenues are generally less than 100 k€ per year per MW installed. Similarly to our economic analysis, this is far from enough to justify the investment in utility-scale batteries. Interestingly, the increased attractiveness of 2021 is mainly due to the energy crisis and not the increased penetration of renewables7.

Aligned with previous calculations, SPglobal calculates for California: Assuming a four-hour battery storage system, the annual revenue accumulated from the top four hours' prices minus the four bottom hours' prices of each day, or TB4, increases up to $55/kW-year by 2030. If we compare these revenues with the following announcement of a 500 M$ investment for 255 MW/1 GWh, or 1960 $ per kW for a 4-hour battery, it is clear that arbitrage only is unlikely to justify the investment.

What about smaller batteries?

The majority of batteries in terms of energy content are actually used in electric vehicles. In Germany, the energy content of all the batteries is about to reach the level of storing one hour of the maximal solar output (71 GW).

Electric vehicles could provide some relief when there is a real energy surplus but it is unlikely that they will be used to do real energy arbitrage (buy and sell energy). It is much more likely that people will charge them when prices are low, provided that tariffs are adjusted accordingly8. In addition, these batteries could provide grid services such as power reserves when connected to the charging points.

So, for what do we need large-scale batteries?

Even though large-scale stationary batteries are unlikely to provide price arbitrage in the day-ahead markets in the coming years, they are still useful, especially with the increased penetration of renewables. Various applications are well-served by them such as (read this post for a more extensive overview):

Power reserves. Currently, most utility-scale batteries are providing FCR (Frequency Containment Reserves) and they will gain market share in other power reserves such as aFRR (automatic Frequency Restoration Reserves).

Other grid support products such as voltage regulation, black start, or congestion management.

Portfolio optimization with regard to imbalances and intraday markets. Imbalance prices and to a lesser extent intraday markets are much more volatile than day-ahead markets.

In conclusion

The integration of renewables is requiring innovative technologies and utility-scale batteries are one of them. In the coming years, such batteries will provide grid services and very-short term portfolio optimization but it is unlikely that they will be used to reduce the volatility on the day-ahead exchanges. With the solar revolution on its way, market prices will be confronted more and more with the “canyon curve”.

Nevertheless, the demand response from the electrification of transportation could partly be a solution to limit the extremely low prices but only if tariffs are incentivizing consumers to use the cheap energy when prices are low. In addition, due to the current speed of solar installation across the EU, it is likely that curtailment of renewables will become more frequent as the system would not be able to provide the necessary flexibility needed. And finally, pumped-hydro, the traditional grid-scale storage, would be increasingly more interesting.

From a recent study on Energy Storage by EnTEC: The annual European energy storage market for stationary batteries in the electricity system has seen an increase in installed capacity from 0.6 GWh in 2015 to about 9.4 GWh in 2022. Between 2021 and 2022 the market has doubled. About 30% of the 2022 market was residential storage, roughly 2% was Commercial and Industrial (C&I) storage, and about 70% were front-of-meter installations. It should be noted that 9.4 GWh is the equivalent of fewer than 2 minutes of total electricity consumption in the EU. In addition, pumped hydro storage (PHS) is still dominant with a stored energy of around 200 GWh.

Estimated at 209 GW at the end of 2022 in the EU.

750 GW DC side or the equivalent of 600 GW AC side.

And for the coming years. In 2030 and after, it would depend on technological advancement.

Except during the energy crisis in 2021 and 2022, a price spread of 100 EUR/MWh for 4 consecutive hours almost every day of the year is unlikely.

It is like installing a large gas power plant. The power plant will bid into the balancing markets for example, yet the primary objective is to make revenue from the energy markets (day-ahead and long-term).

When natural gas is more expensive, the price of the peak hours is much more expensive as gas power plants are the ones setting the price, increasing greatly the spread, even if the lowest daily prices are not zero.

Thanks for another interesting article!

Looking at the Duration/Frequency graph showing the best technology at each point, I am wondering what the graph would look like when omitting Pumped Hydro. Namely as in certain regions (e.g. The Netherlands) Pumped Hydro is not an option, or otherwise more costly, due to the absence of height differences in the natural landscape. Do you happen to know of such graph?