Heatwave on Europe: the impact of a "Hitzeflaute"

As a heat wave has engulfed Europe, there is a new sexy word in the European energy world: Hitzeflaute1, which is an updated version of the Dunkelflaute2, but for a hot summer day. Let’s discover together the impact of the heatwave on the European power markets!

The recent heatwave

Europe has experienced a serious heatwave with Paris reaching 40 degrees on Tuesday 1 July.

Unsurprisingly, the heatwave has directly impacted electricity spot prices due to the following reasons (not exhaustive):

Increased Demand: The primary cause is the heightened demand for air conditioning. With a growing number of heat pumps, European power demand is likely to be increasingly affected by high temperatures. Additionally, demand remains relatively high for air conditioning in the evening when solar generation is low.

Reduced Power Plant Output: Some power plants cannot operate at maximum capacity during extreme heat, and others may be unable to run due to environmental constraints, such as excessively high cooling water temperatures (in rivers).

Scheduled Maintenance: Several power plants have annual maintenance planned for the summer months, as demand is generally lower.

In these conditions, with minimal renewable generation available, including wind, day-ahead prices surged to 517.57 €/MWh in Belgium and the Netherlands, followed by Germany and Denmark at 476.19 €/MWh at 8 PM on July 1st.

Dunkelflaute vs Hitzeflaute

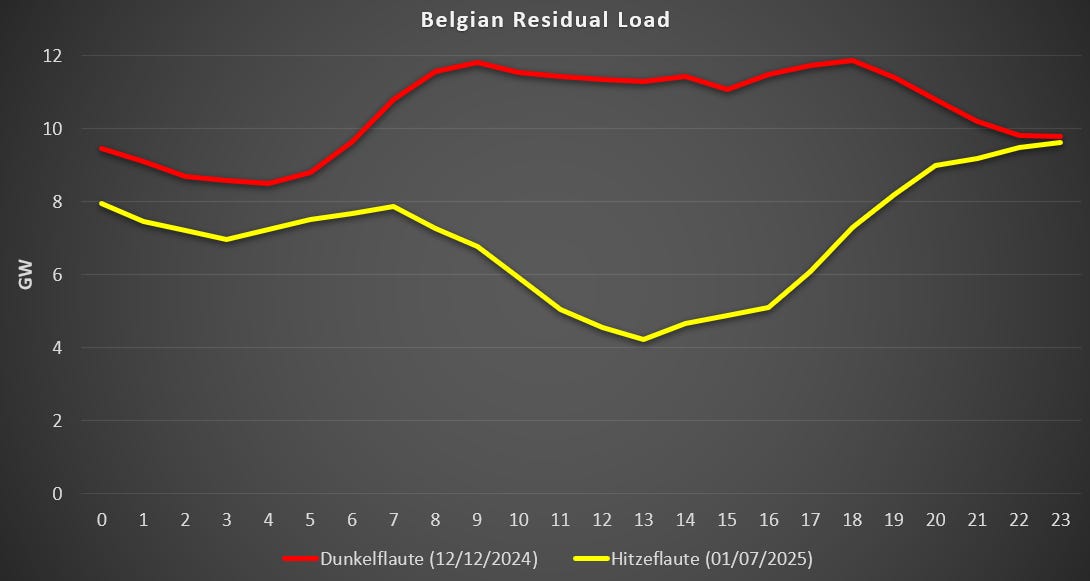

Such a situation of high demand and low renewables happen generally in the winter, in the so-called Dunkelfalute period. Hereunder are the graphs of the day-ahead price, the renewable generation, and the residual load in Belgium for the 12 December 2024 and the 1 July 2025.

There are obvious differences between these two days:

The residual load stays high most of the day during a Dunkelflaute day, reflecting the fact that virtually no renewable is present. During a Hitzeflaute, this is very different as solar generation is reaching confortable level.

The market prices stay high for the red curve (12 consecutive hours above 300 €/MWh), while the yellow curve shows only a relatively peak (only 4 hours above 300 €/MWh).

The recent episode has really shown that the scarcity is only for a few hours, while the other one was due to a much longer scarcity. The potential solutions to cope with such events are therefore quite different:

For the Hitzeflaute, flexibility is really key, together with solar. Increasing load shifting and storage would flatten the curve, rendering the situation more manageable.

For the Dunkelflaute, short-term flexibility won’t be sufficient as the scarcity is lasting more than a day. Simply expanding renewable infrastructure won't significantly alter the situation, as both wind and solar outputs are minimal. On such days, increased transmission—drawing on potential generation from neighboring countries—could be beneficial, although low renewable output might affect a broader area. The true solution lies in developing longer-term storage solutions3, although viable and economical options have yet to emerge.

This situation occurred already last year

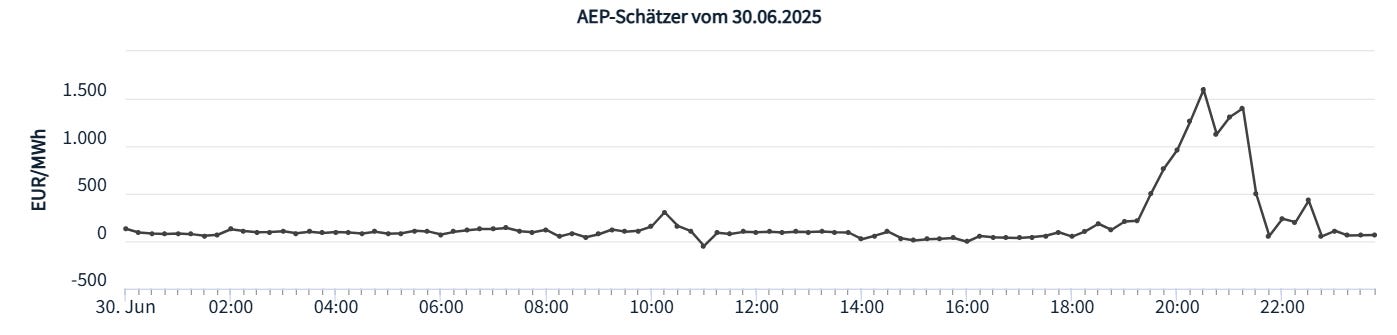

Such high prices on the day-ahead markets already happened last year in other countries, notably in Eastern Europe. Hereunder is the graph of the day-ahead prices of Hungary. Prices reached up to 1000 €/MWh in some hours.

This has led to some of the highest daily spreads4, even higher than during the energy crisis in 2022, with 30-days rolling average of the daily spread of more than 400 €/MWh.

Even though I focus my posts on Europe, such heatwaves have a similar impact on the other side of the Atlantic as well as we can see in this animation.

Consequences on balancing capacity

The heatwave has also a direct consequence on the prices of balancing capacity5. Hereunder are the average capacity prices for the 1st July for Germany6. The first graph shows the upward direction and the second one shows the downward direction.

The following observations can be made:

Downward Direction: The balancing prices for both aFRR and mFRR are closely correlated with solar generation. This phenomenon has been described in previous posts.

Upward Direction:

aFRR: There are higher prices for the daytime blocks, with capacity prices exceeding 20 €/MW/h for three blocks during the day (8-12, 12-16, and 16-20).

mFRR: Prices are negligible during the day, especially at the solar peak (12-16). However, capacity prices rise significantly during the evening peak, aligning with peak prices on the day-ahead market. Notably, the average mFRR capacity price for this peak block is higher than the average aFRR capacity price.

Imbalance prices - Tuesday 1 July

We can also examine the imbalance prices across various countries. Although the calculation methods for these prices vary significantly between countries, we can see that during the evening, a large region was experiencing high imbalance prices at the same time7. Below is a snapshot from the platform balancing.services, an excellent resource for all things related to the European balancing market.

Looking closer to Germany, we saw price spiking in intraday, and consequently also in the imbalance price. Hereunder for more precision on that matter from Montel Analytics.

Imbalance prices - Monday 30 June

The imbalance prices observed on Monday, June 30, were also quite high. One key element has been the aFRR energy price, also known as cross-border marginal prices, since numerous countries are now part of the European platform Picasso.

The central concept is that when transmission capacity is available, aFRR balancing energy can be exchanged, leading to equal aFRR activation prices (or CBMP). Below is the graph depicting CBMP aFRR for Germany, Belgium, France, and Germany over three consecutive hours.

We can observe that prices were converging well at 7 PM. Later, during the night, France experienced consistently lower prices. At one point, there was a significant surge in the CBMP for Belgium and the Netherlands, reaching 3990 €/MWh and sustained over 1895 €/MWh for more than 30 minutes. These activation prices directly impacted the imbalance prices, although they are not the only component of the imbalance pricing8.

In Germany as well, the imbalance price has been elevated at the same moment, even though the imbalance price at that moment was not directly due to the aFRR activations but from the intraday index9.

In conclusion

As a conclusion, I would refer to this article and cites the last two paragraphs:

Europe’s power system is now shaped as much by climate as by technology. Heatwaves are no longer rare disruptions but regular, systemic stress tests. Each year, the margin for error narrows.

The paradox of abundant solar energy by day and high-cost scarcity by night is becoming structural. The system must evolve to match supply and demand in real time, pairing each shape with the right slot. The price signals are clear. The challenge is putting the right tools to the right tasks – before the toy breaks.

As illustrated in the graphs above, increased demand during a heatwave strains the grid, leading to elevated prices. In such scenarios, disturbances can have even greater impacts as the system is already under pressure. However, just a few hours earlier, the system benefited from abundant solar energy. Therefore, the logical solution seems to push for appropriate regulation and technology to flatten the curve.

Thanks for reading!

Julien

I first saw this word in a post of Montel Analytics.

See my former post on the Dunkelflaute.

Storage from one week to another, for example, or even seasonal storage.

The daily spread is defined as the difference between the maximal and the minimal price of the day.

For aFRR, it is for Germany and Austria combined, and for mFRR, it is only for Germany.

Imbalance prices change every 15 minutes.

In Belgium notably, for these hours, the mFRR activation price has also led to high imbalance price on 30 June.

Very good post as always ! Do you know who made balancing.services ? (very nice too 😄)

As usual, a fine post. Addressing the "more a/c but no PV after sunset" this is a trivial problem to solve. Indeed it was solved by a US company with a system they called “Ice-Bear”. In summary – use PV to power both the A/c and cold storage. Sun goes down, cold store takes over. Works well. Problem is, elec markets can’t/won’t drive the uptake of this tech. As for this comment:

“Europe’s power system is now shaped as much by climate as by technology. Heatwaves are no longer rare disruptions but regular, systemic stress tests..” The problem is that marginal markets were an answer to a fossil past, we now face a weather define future & marginal markets – as the price oscillations show deliver signals that are useless for investment purposes.

Indeed, what passes for thinking in EU institutions is that massive price oscillations are not a system malfunction they are a feature – which, marginal market believers thinks, will deliver system responses/change. This childish thinking is disproved by empirical reality – show me all the storage, the a/c cold stores, the medium/long term storage. None. A solution demands two actions: price energy at cost not “at the margin” which in any case is a category error/circular thinking, two engineer storage of various sorts & then use markets to cost optimise operation. This would be the sensible way, but it won’t happen because – from an EU institutional PoV “markets rule Ok & have all the answers” – meanwhile, increasingly, the TSOs pick up the pieces. Clever.